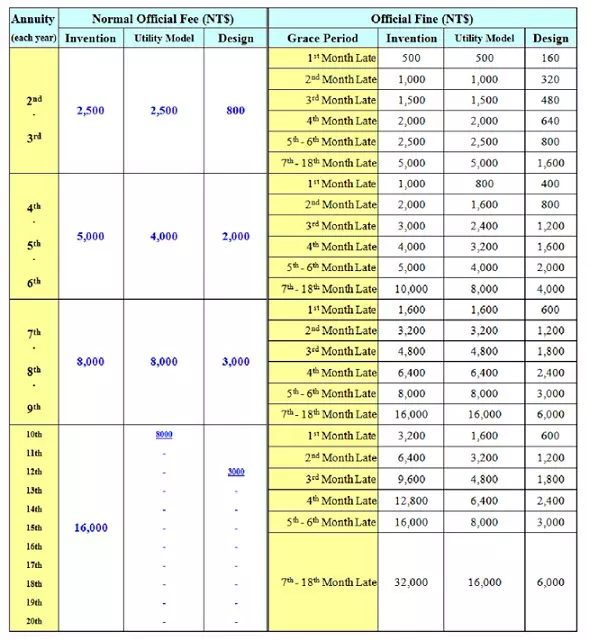

OFFICIAL FEE SCHEDULE FOR TAIWAN PATENT ANNUITY

Remark:

- The above fee schedule does not include the agent’s fee for attending to each of the annuities.

- The grace period for late payment of annuities is one and half (1 1/2) year from the original due date, provided that a 20% surcharge fine will be incurred if the late payment is made within one (1) month from the due date, a 40%, 60%, 80% and 100% surcharge fine will be incurred if late payment is made within two (2) months, three (3) months, four (4) months and five-six (5-6) months, respectively. Whereas a 200% surcharge fine will be incurred if the late payment is made within 7th to 18th months from the original due date.

- For a natural person, school or small/medium enterprises applicant, for 1st to 3rd patent annuities, a NT$800/each year of official annuity fee could be deducted; and for 4th to 6th patent annuities, a NT$1200/each year of official annuity fee could be deducted. As to the amount of surcharge fine for the late payment within the grace period, for the applicant who could enjoy reduction of payment of patent annuity the surcharge fine percentage will be determined per the calculation manner as mentioned in the above item 2 of this Remark.